Subpart D - Risk-Weighted Assets - Standardized Approach

§ 324.30 Applicability.

(a) This subpart sets forth methodologies for determining risk-weighted assets for purposes of the generally applicable risk-based capital requirements for all FDIC-supervised institutions.

(b) Notwithstanding paragraph (a) of this section, a market risk FDIC-supervised institution must exclude from its calculation of risk-weighted assets under this subpart the risk-weighted asset amounts of all covered positions, as defined in subpart F of this part (except foreign exchange positions that are not trading positions, OTC derivative positions, cleared transactions, and unsettled transactions).

Risk-Weighted Assets for General Credit Risk

§ 324.31 Mechanics for calculating risk-weighted assets for general credit risk.

(a) General risk-weighting requirements. An FDIC-supervised institution must apply risk weights to its exposures as follows:

(1) An FDIC-supervised institution must determine the exposure amount of each on-balance sheet exposure, each OTC derivative contract, and each off-balance sheet commitment, trade and transaction-related contingency, guarantee, repo-style transaction, financial standby letter of credit, forward agreement, or other similar transaction that is not:

(i) An unsettled transaction subject to § 324.38;

(ii) A cleared transaction subject to § 324.35;

(iii) A default fund contribution subject to § 324.35;

(2) The FDIC-supervised institution must multiply each exposure amount by the risk weight appropriate to the exposure based on the exposure type or counterparty, eligible guarantor, or financial collateral to determine the risk-weighted asset amount for each exposure.

(b) Total risk-weighted assets for general credit risk equals the sum of the risk-weighted asset amounts calculated under this section.

§ 324.32 General risk weights.

(a) Sovereign exposures —

(1) Exposures to the U.S. government.

(i) Notwithstanding any other requirement in this subpart, an FDIC-supervised institution must assign a zero percent risk weight to:

(A) An exposure to the U.S. government, its central bank, or a U.S. government agency; and

(B) The portion of an exposure that is directly and unconditionally guaranteed by the U.S. government, its central bank, or a U.S. government agency. This includes a deposit or other exposure, or the portion of a deposit or other exposure, that is insured or otherwise unconditionally guaranteed by the FDIC or National Credit Union Administration.

(ii) An FDIC-supervised institution must assign a 20 percent risk weight to the portion of an exposure that is conditionally guaranteed by the U.S. government, its central bank, or a U.S. government agency. This includes an exposure, or the portion of an exposure, that is conditionally guaranteed by the FDIC or National Credit Union Administration.

(iii) An FDIC-supervised institution must assign a zero percent risk weight to a Paycheck Protection Program covered loan as defined in section 7(a)(36) of the Small Business Act (15 U.S.C. 636(a)(36)).

(2) Other sovereign exposures. In accordance with Table 1 to § 324.32, an FDIC-supervised institution must assign a risk weight to a sovereign exposure based on the CRC applicable to the sovereign or the sovereign's OECD membership status if there is no CRC applicable to the sovereign.

Table 1 to § 324.32—Risk Weights for Sovereign Exposures

| Risk Weight (in percent) |

||

| CRC | 0-1 | 0 |

| 2 | 20 | |

| 3 | 50 | |

| 4-6 | 100 | |

| 7 | 150 | |

| OECD Member with No CRC | 0 | |

| Non-OECD Member with No CRC | 100 | |

| Sovereign Default | 150 | |

(3) Certain sovereign exposures. Notwithstanding paragraph (a)(2) of this section, an FDIC-supervised institution may assign to a sovereign exposure a risk weight that is lower than the applicable risk weight in Table 1 to § 324.32 if:

(i) The exposure is denominated in the sovereign's currency;

(ii) The FDIC-supervised institution has at least an equivalent amount of liabilities in that currency; and

(iii) The risk weight is not lower than the risk weight that the home country supervisor allows FDIC-supervised institutions under its jurisdiction to assign to the same exposures to the sovereign.

(4) Exposures to a non-OECD member sovereign with no CRC. Except as provided in paragraphs (a)(3), (a)(5) and (a)(6) of this section, an FDIC-supervised institution must assign a 100 percent risk weight to an exposure to a sovereign if the sovereign does not have a CRC.

(5) Exposures to an OECD member sovereign with no CRC. Except as provided in paragraph (a)(6) of this section, an FDIC-supervised institution must assign a 0 percent risk weight to an exposure to a sovereign that is a member of the OECD if the sovereign does not have a CRC.

(6) Sovereign default. An FDIC-supervised institution must assign a 150 percent risk weight to a sovereign exposure immediately upon determining that an event of sovereign default has occurred, or if an event of sovereign default has occurred during the previous five years.

(b) Certain supranational entities and multilateral development banks (MDBs). An FDIC-supervised institution must assign a zero percent risk weight to an exposure to the Bank for International Settlements, the European Central Bank, the European Commission, the International Monetary Fund, the European Stability Mechanism, the European Financial Stability Facility, or an MDB.

(c) Exposures to GSEs.

(1) An FDIC-supervised institution must assign a 20 percent risk weight to an exposure to a GSE other than an equity exposure or preferred stock.

(2) An FDIC-supervised institution must assign a 100 percent risk weight to preferred stock issued by a GSE.

(d) Exposures to depository institutions, foreign banks, and credit unions —

(1) Exposures to U.S. depository institutions and credit unions. An FDIC-supervised institution must assign a 20 percent risk weight to an exposure to a depository institution or credit union that is organized under the laws of the United States or any state thereof, except as otherwise provided under paragraph (d)(3) of this section.

(2) Exposures to foreign banks.

(i) Except as otherwise provided under paragraphs (d)(2)(iii), (d)(2)(v), and (d)(3) of this section, an FDIC-supervised institution must assign a risk weight to an exposure to a foreign bank, in accordance with Table 2 to § 324.32, based on the CRC that corresponds to the foreign bank's home country or the OECD membership status of the foreign bank's home country if there is no CRC applicable to the foreign bank's home country.

Table 2 to § 324.32—Risk Weights for Exposures to Foreign Banks

| Risk weight (in percent) |

|

|---|---|

| CRC: | |

| 0-1 | 20 |

| 2 | 50 |

| 3 | 100 |

| 4-7 | 150 |

| OECD Member with No CRC | 20 |

| Non-OECD Member with No CRC | 100 |

| Sovereign Default | 150 |

(ii) An FDIC-supervised institution must assign a 20 percent risk weight to an exposure to a foreign bank whose home country is a member of the OECD and does not have a CRC.

(iii) An FDIC-supervised institution must assign a 20 percent risk-weight to an exposure that is a self-liquidating, trade-related contingent item that arises from the movement of goods and that has a maturity of three months or less to a foreign bank whose home country has a CRC of 0, 1, 2, or 3, or is an OECD member with no CRC.

(iv) An FDIC-supervised institution must assign a 100 percent risk weight to an exposure to a foreign bank whose home country is not a member of the OECD and does not have a CRC, with the exception of self-liquidating, trade-related contingent items that arise from the movement of goods, and that have a maturity of three months or less, which may be assigned a 20 percent risk weight.

(v) An FDIC-supervised institution must assign a 150 percent risk weight to an exposure to a foreign bank immediately upon determining that an event of sovereign default has occurred in the bank's home country, or if an event of sovereign default has occurred in the foreign bank's home country during the previous five years.

(3) An FDIC-supervised institution must assign a 100 percent risk weight to an exposure to a financial institution if the exposure may be included in that financial institution's capital unless the exposure is:

(i) An equity exposure;

(ii) A significant investment in the capital of an unconsolidated financial institution in the form of common stock pursuant to § 324.22(d)(2)(i)(c);

(iii) Deducted from regulatory capital under § 324.22; or

(iv) Subject to a 150 percent risk weight under paragraph (d)(2)(iv) or Table 2 of paragraph (d)(2) of this section.

(e) Exposures to public sector entities (PSEs) —

(1) Exposures to U.S. PSEs.

(i) An FDIC-supervised institution must assign a 20 percent risk weight to a general obligation exposure to a PSE that is organized under the laws of the United States or any state or political subdivision thereof.

(ii) An FDIC-supervised institution must assign a 50 percent risk weight to a revenue obligation exposure to a PSE that is organized under the laws of the United States or any state or political subdivision thereof.

(2) Exposures to foreign PSEs.

(i) Except as provided in paragraphs (e)(1) and (e)(3) of this section, an FDIC-supervised institution must assign a risk weight to a general obligation exposure to a PSE, in accordance with Table 3 to § 324.32, based on the CRC that corresponds to the PSE's home country or the OECD membership status of the PSE's home country if there is no CRC applicable to the PSE's home country.

(ii) Except as provided in paragraphs (e)(1) and (e)(3) of this section, an FDIC-supervised institution must assign a risk weight to a revenue obligation exposure to a PSE, in accordance with Table 4 to § 324.32, based on the CRC that corresponds to the PSE's home country; or the OECD membership status of the PSE's home country if there is no CRC applicable to the PSE's home country.

(3) An FDIC-supervised institution may assign a lower risk weight than would otherwise apply under Tables 3 or 4 to § 324.32 to an exposure to a foreign PSE if:

(i) The PSE's home country supervisor allows banks under its jurisdiction to assign a lower risk weight to such exposures; and

(ii) The risk weight is not lower than the risk weight that corresponds to the PSE's home country in accordance with Table 1 to § 324.32.

Table 3 to § 324.32—Risk Weights for non-U.S. PSE General Obligations

| Risk Weight (in percent) |

||

| CRC | 0-1 | 20 |

| 2 | 50 | |

| 3 | 100 | |

| 4-7 | 150 | |

| OECD Member with No CRC | 20 | |

| Non-OECD Member with No CRC | 100 | |

| Sovereign Default | 150 | |

Table 4 to § 324.32—Risk Weights for non-U.S. PSE Revenue Obligations

| Risk Weight (in percent) |

||

| CRC | 0-1 | 50 |

| 2-3 | 50 | |

| 4-7 | 150 | |

| OECD Member with No CRC | 50 | |

| Non-OECD Member with No CRC | 100 | |

| Sovereign Default | 150 | |

(4) Exposures to PSEs from an OECD member sovereign with no CRC.

(i) An FDIC-supervised institution must assign a 20 percent risk weight to a general obligation exposure to a PSE whose home country is an OECD member sovereign with no CRC.

(ii) An FDIC-supervised institution must assign a 50 percent risk weight to a revenue obligation exposure to a PSE whose home country is an OECD member sovereign with no CRC.

(5) Exposures to PSEs whose home country is not an OECD member sovereign with no CRC. An FDIC-supervised institution must assign a 100 percent risk weight to an exposure to a PSE whose home country is not a member of the OECD and does not have a CRC.

(6) An FDIC-supervised institution must assign a 150 percent risk weight to a PSE exposure immediately upon determining that an event of sovereign default has occurred in a PSE's home country or if an event of sovereign default has occurred in the PSE's home country during the previous five years.

(f) Corporate exposures.

(1) An FDIC-supervised institution must assign a 100 percent risk weight to all its corporate exposures, except as provided in paragraphs (f)(2) and (f)(3) of this section.

(2) A FDIC-supervised institution must assign a 2 percent risk weight to an exposure to a QCCP arising from the FDIC-supervised institution posting cash collateral to the QCCP in connection with a cleared transaction that meets the requirements of § 324.35(b)(3)(i)(A) and a 4 percent risk weight to an exposure to a QCCP arising from the FDIC-supervised institution posting cash collateral to the QCCP in connection with a cleared transaction that meets the requirements of § 324.35(b)(3)(i)(B).

(3) A FDIC-supervised institution must assign a 2 percent risk weight to an exposure to a QCCP arising from the FDIC-supervised institution posting cash collateral to the QCCP in connection with a cleared transaction that meets the requirements of § 324.35(c)(3)(i).

(g) Residential mortgage exposures.

(1) An FDIC-supervised institution must assign a 50 percent risk weight to a first-lien residential mortgage exposure that:

(i) Is secured by a property that is either owner-occupied or rented;

(ii) Is made in accordance with prudent underwriting standards, including standards relating to the loan amount as a percent of the appraised value of the property;

(iii) Is not 90 days or more past due or carried in nonaccrual status; and

(iv) Is not restructured or modified.

(2) An FDIC-supervised institution must assign a 100 percent risk weight to a first-lien residential mortgage exposure that does not meet the criteria in paragraph (g)(1) of this section, and to junior-lien residential mortgage exposures.

(3) For the purpose of this paragraph (g), if an FDIC-supervised institution holds the first-lien and junior-lien(s) residential mortgage exposures, and no other party holds an intervening lien, the FDIC-supervised institution must combine the exposures and treat them as a single first-lien residential mortgage exposure.

(4) A loan modified or restructured solely pursuant to the U.S. Treasury's Home Affordable Mortgage Program is not modified or restructured for purposes of this section.

(h) Pre-sold construction loans. An FDIC-supervised institution must assign a 50 percent risk weight to a pre-sold construction loan unless the purchase contract is cancelled, in which case an FDIC-supervised institution must assign a 100 percent risk weight.

(i) Statutory multifamily mortgages. An FDIC-supervised institution must assign a 50 percent risk weight to a statutory multifamily mortgage.

(j) High-volatility commercial real estate (HVCRE) exposures. An FDIC-supervised institution must assign a 150 percent risk weight to an HVCRE exposure.

(k) Past due exposures. Except for an exposure to a sovereign entity or a residential mortgage exposure or a policy loan, if an exposure is 90 days or more past due or on nonaccrual:

(1) An FDIC-supervised institution must assign a 150 percent risk weight to the portion of the exposure that is not guaranteed or that is unsecured;

(2) An FDIC-supervised institution may assign a risk weight to the guaranteed portion of a past due exposure based on the risk weight that applies under § 324.36 if the guarantee or credit derivative meets the requirements of that section; and

(3) An FDIC-supervised institution may assign a risk weight to the collateralized portion of a past due exposure based on the risk weight that applies under § 324.37 if the collateral meets the requirements of that section.

(l) Other assets.

(1) An FDIC-supervised institution must assign a zero percent risk weight to cash owned and held in all offices of the FDIC-supervised institution or in transit; to gold bullion held in the FDIC-supervised institution's own vaults or held in another depository institution's vaults on an allocated basis, to the extent the gold bullion assets are offset by gold bullion liabilities; and to exposures that arise from the settlement of cash transactions (such as equities, fixed income, spot foreign exchange and spot commodities) with a central counterparty where there is no assumption of ongoing counterparty credit risk by the central counterparty after settlement of the trade and associated default fund contributions.

(2) An FDIC-supervised institution must assign a 20 percent risk weight to cash items in the process of collection.

(3) An FDIC-supervised institution must assign a 100 percent risk weight to DTAs arising from temporary differences that the FDIC-supervised institution could realize through net operating loss carrybacks.

(4) An FDIC-supervised institution must assign a 250 percent risk weight to the portion of each of the following items to the extent it is not deducted from common equity tier 1 capital pursuant to § 324.22(d):

(i) MSAs; and

(ii) DTAs arising from temporary differences that the FDIC-supervised institution could not realize through net operating loss carrybacks.

(5) An FDIC-supervised institution must assign a 100 percent risk weight to all assets not specifically assigned a different risk weight under this subpart and that are not deducted from tier 1 or tier 2 capital pursuant to § 324.22.

(6) Notwithstanding the requirements of this section, an FDIC-supervised institution may assign an asset that is not included in one of the categories provided in this section to the risk weight category applicable under the capital rules applicable to bank holding companies and savings and loan holding companies under 12 CFR part 217, provided that all of the following conditions apply:

(i) The FDIC-supervised institution is not authorized to hold the asset under applicable law other than debt previously contracted or similar authority; and

(ii) The risks associated with the asset are substantially similar to the risks of assets that are otherwise assigned to a risk weight category of less than 100 percent under this subpart.

[78 FR 55471, Sept. 10, 2013, as amended at 79 FR 20759, Apr. 14, 2014; 84 FR 35275, July 22, 2019; 85 FR 4431, Jan. 24, 2020; 85 FR 20394, Apr. 13, 2020; 85 FR 57963, Sept. 17, 2020]

§ 324.33 Off-balance sheet exposures.

(a) General.

(1) An FDIC-supervised institution must calculate the exposure amount of an off-balance sheet exposure using the credit conversion factors (CCFs) in paragraph (b) of this section.

(2) Where an FDIC-supervised institution commits to provide a commitment, the FDIC-supervised institution may apply the lower of the two applicable CCFs.

(3) Where an FDIC-supervised institution provides a commitment structured as a syndication or participation, the FDIC-supervised institution is only required to calculate the exposure amount for its pro rata share of the commitment.

(4) Where an FDIC-supervised institution provides a commitment, enters into a repurchase agreement, or provides a credit-enhancing representation and warranty, and such commitment, repurchase agreement, or credit-enhancing representation and warranty is not a securitization exposure, the exposure amount shall be no greater than the maximum contractual amount of the commitment, repurchase agreement, or credit-enhancing representation and warranty, as applicable.

(b) Credit conversion factors —

(1) Zero percent CCF. An FDIC-supervised institution must apply a zero percent CCF to the unused portion of a commitment that is unconditionally cancelable by the FDIC-supervised institution.

(2) 20 percent CCF. An FDIC-supervised institution must apply a 20 percent CCF to the amount of:

(i) Commitments with an original maturity of one year or less that are not unconditionally cancelable by the FDIC-supervised institution; and

(ii) Self-liquidating, trade-related contingent items that arise from the movement of goods, with an original maturity of one year or less.

(3) 50 percent CCF. An FDIC-supervised institution must apply a 50 percent CCF to the amount of:

(i) Commitments with an original maturity of more than one year that are not unconditionally cancelable by the FDIC-supervised institution; and

(ii) Transaction-related contingent items, including performance bonds, bid bonds, warranties, and performance standby letters of credit.

(4) 100 percent CCF. An FDIC-supervised institution must apply a 100 percent CCF to the amount of the following off-balance-sheet items and other similar transactions:

(i) Guarantees;

(ii) Repurchase agreements (the off-balance sheet component of which equals the sum of the current fair values of all positions the FDIC-supervised institution has sold subject to repurchase);

(iii) Credit-enhancing representations and warranties that are not securitization exposures;

(iv) Off-balance sheet securities lending transactions (the off-balance sheet component of which equals the sum of the current fair values of all positions the FDIC-supervised institution has lent under the transaction);

(v) Off-balance sheet securities borrowing transactions (the off-balance sheet component of which equals the sum of the current fair values of all non-cash positions the FDIC-supervised institution has posted as collateral under the transaction);

(vi) Financial standby letters of credit; and

(vii) Forward agreements.

§ 324.34 Derivative contracts.

(a) Exposure amount for derivative contracts —

(1) FDIC-supervised institution that is not an advanced approaches FDIC-supervised institution.

(i) A FDIC-supervised institution that is not an advanced approaches FDIC-supervised institution must use the current exposure methodology (CEM) described in paragraph (b) of this section to calculate the exposure amount for all its OTC derivative contracts, unless the FDIC-supervised institution makes the election provided in paragraph (a)(1)(ii) of this section.

(ii) A FDIC-supervised institution that is not an advanced approaches FDIC-supervised institution may elect to calculate the exposure amount for all its OTC derivative contracts under the standardized approach for counterparty credit risk (SA-CCR) in § 324.132(c) by notifying the FDIC, rather than calculating the exposure amount for all its derivative contracts using CEM. A FDIC-supervised institution that elects under this paragraph (a)(1)(ii) to calculate the exposure amount for its OTC derivative contracts under SA-CCR must apply the treatment of cleared transactions under § 324.133 to its derivative contracts that are cleared transactions and to all default fund contributions associated with such derivative contracts, rather than applying § 324.35. A FDIC-supervised institution that is not an advanced approaches FDIC-supervised institution must use the same methodology to calculate the exposure amount for all its derivative contracts and, if a FDIC-supervised institution has elected to use SA-CCR under this paragraph (a)(1)(ii), the FDIC-supervised institution may change its election only with prior approval of the FDIC.

(2) Advanced approaches FDIC-supervised institution. An advanced approaches FDIC-supervised institution must calculate the exposure amount for all its derivative contracts using SA-CCR in § 324.132(c) for purposes of standardized total risk-weighted assets. An advanced approaches FDIC-supervised institution must apply the treatment of cleared transactions under § 324.133 to its derivative contracts that are cleared transactions and to all default fund contributions associated with such derivative contracts for purposes of standardized total risk-weighted assets.

(b) Current exposure methodology exposure amount —

(1) Single OTC derivative contract. Except as modified by paragraph (c) of this section, the exposure amount for a single OTC derivative contract that is not subject to a qualifying master netting agreement is equal to the sum of the FDIC-supervised institution's current credit exposure and potential future credit exposure (PFE) on the OTC derivative contract.

(i) Current credit exposure. The current credit exposure for a single OTC derivative contract is the greater of the fair value of the OTC derivative contract or zero.

(ii) PFE.

(A) The PFE for a single OTC derivative contract, including an OTC derivative contract with a negative fair value, is calculated by multiplying the notional principal amount of the OTC derivative contract by the appropriate conversion factor in Table 1 to this section.

(B) For purposes of calculating either the PFE under this paragraph (b)(1)(ii) or the gross PFE under paragraph (b)(2)(ii)(A) of this section for exchange rate contracts and other similar contracts in which the notional principal amount is equivalent to the cash flows, notional principal amount is the net receipts to each party falling due on each value date in each currency.

(C) For an OTC derivative contract that does not fall within one of the specified categories in Table 1 to this section, the PFE must be calculated using the appropriate “other” conversion factor.

(D) A FDIC-supervised institution must use an OTC derivative contract's effective notional principal amount (that is, the apparent or stated notional principal amount multiplied by any multiplier in the OTC derivative contract) rather than the apparent or stated notional principal amount in calculating PFE.

(E) The PFE of the protection provider of a credit derivative is capped at the net present value of the amount of unpaid premiums.

Table 1 to § 324.34—Conversion Factor Matrix for Derivative Contracts 1

| Remaining maturity 2 | Interest rate | Foreign exchange rate and gold |

Credit (investment grade reference asset) 3 |

Credit (non-investment- grade reference asset) |

Equity | Precious metals (except gold) |

Other |

|---|---|---|---|---|---|---|---|

| One year or less | 0.00 | 0.01 | 0.05 | 0.10 | 0.06 | 0.07 | 0.10 |

| Greater than one year and less than or equal to five years | 0.005 | 0.05 | 0.05 | 0.10 | 0.08 | 0.07 | 0.12 |

| Greater than five years | 0.015 | 0.075 | 0.05 | 0.10 | 0.10 | 0.08 | 0.15 |

(2) Multiple OTC derivative contracts subject to a qualifying master netting agreement. Except as modified by paragraph (c) of this section, the exposure amount for multiple OTC derivative contracts subject to a qualifying master netting agreement is equal to the sum of the net current credit exposure and the adjusted sum of the PFE amounts for all OTC derivative contracts subject to the qualifying master netting agreement.

(i) Net current credit exposure. The net current credit exposure is the greater of the net sum of all positive and negative fair values of the individual OTC derivative contracts subject to the qualifying master netting agreement or zero.

(ii) Adjusted sum of the PFE amounts. The adjusted sum of the PFE amounts, Anet, is calculated as Anet = (0.4 × Agross) + (0.6 × NGR × Agross), where:

(A) Agross = the gross PFE (that is, the sum of the PFE amounts as determined under paragraph (b)(1)(ii) of this section for each individual derivative contract subject to the qualifying master netting agreement); and

(B) Net-to-gross Ratio (NGR) = the ratio of the net current credit exposure to the gross current credit exposure. In calculating the NGR, the gross current credit exposure equals the sum of the positive current credit exposures (as determined under paragraph (b)(1)(i) of this section) of all individual derivative contracts subject to the qualifying master netting agreement.

(c) Recognition of credit risk mitigation of collateralized OTC derivative contracts.

(1) A FDIC-supervised institution using CEM under paragraph (b) of this section may recognize the credit risk mitigation benefits of financial collateral that secures an OTC derivative contract or multiple OTC derivative contracts subject to a qualifying master netting agreement (netting set) by using the simple approach in § 324.37(b).

(2) As an alternative to the simple approach, a FDIC-supervised institution using CEM under paragraph (b) of this section may recognize the credit risk mitigation benefits of financial collateral that secures such a contract or netting set if the financial collateral is marked-to-fair value on a daily basis and subject to a daily margin maintenance requirement by applying a risk weight to the uncollateralized portion of the exposure, after adjusting the exposure amount calculated under paragraph (b)(1) or (2) of this section using the collateral haircut approach in § 324.37(c). The FDIC-supervised institution must substitute the exposure amount calculated under paragraph (b)(1) or (2) of this section for ΣE in the equation in § 324.37(c)(2).

(d) Counterparty credit risk for credit derivatives —

(1) Protection purchasers. A FDIC-supervised institution that purchases a credit derivative that is recognized under § 324.36 as a credit risk mitigant for an exposure that is not a covered position under subpart F of this part is not required to compute a separate counterparty credit risk capital requirement under this subpart provided that the FDIC-supervised institution does so consistently for all such credit derivatives. The FDIC-supervised institution must either include all or exclude all such credit derivatives that are subject to a qualifying master netting agreement from any measure used to determine counterparty credit risk exposure to all relevant counterparties for risk-based capital purposes.

(2) Protection providers.

(i) A FDIC-supervised institution that is the protection provider under a credit derivative must treat the credit derivative as an exposure to the underlying reference asset. The FDIC-supervised institution is not required to compute a counterparty credit risk capital requirement for the credit derivative under this subpart, provided that this treatment is applied consistently for all such credit derivatives. The FDIC-supervised institution must either include all or exclude all such credit derivatives that are subject to a qualifying master netting agreement from any measure used to determine counterparty credit risk exposure.

(ii) The provisions of this paragraph (d)(2) apply to all relevant counterparties for risk-based capital purposes unless the FDIC-supervised institution is treating the credit derivative as a covered position under subpart F of this part, in which case the FDIC-supervised institution must compute a supplemental counterparty credit risk capital requirement under this section.

(e) Counterparty credit risk for equity derivatives.

(1) A FDIC-supervised institution must treat an equity derivative contract as an equity exposure and compute a risk-weighted asset amount for the equity derivative contract under §§ 324.51 through 324.53 (unless the FDIC-supervised institution is treating the contract as a covered position under subpart F of this part).

(2) In addition, the FDIC-supervised institution must also calculate a risk-based capital requirement for the counterparty credit risk of an equity derivative contract under this section if the FDIC-supervised institution is treating the contract as a covered position under subpart F of this part.

(3) If the FDIC-supervised institution risk weights the contract under the Simple Risk-Weight Approach (SRWA) in § 324.52, the FDIC-supervised institution may choose not to hold risk-based capital against the counterparty credit risk of the equity derivative contract, as long as it does so for all such contracts. Where the equity derivative contracts are subject to a qualified master netting agreement, a FDIC-supervised institution using the SRWA must either include all or exclude all of the contracts from any measure used to determine counterparty credit risk exposure.

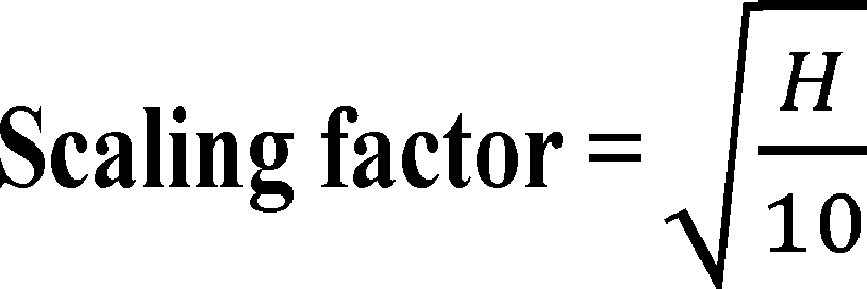

(f) Clearing member FDIC-supervised institution's exposure amount. The exposure amount of a clearing member FDIC-supervised institution using CEM under paragraph (b) of this section for a client-facing derivative transaction or netting set of client-facing derivative transactions equals the exposure amount calculated according to paragraph (b)(1) or (2) of this section multiplied by the scaling factor the square root of 1⁄2 (which equals 0.707107). If the FDIC-supervised institution determines that a longer period is appropriate, the FDIC-supervised institution must use a larger scaling factor to adjust for a longer holding period as follows:

Where H = the holding period greater than or equal to five days. Additionally, the FDIC may require the FDIC-supervised institution to set a longer holding period if the FDIC determines that a longer period is appropriate due to the nature, structure, or characteristics of the transaction or is commensurate with the risks associated with the transaction.

[85 FR 4431, Jan. 24, 2020]

§ 324.35 Cleared transactions.

(a) General requirements —

(1) Clearing member clients. An FDIC-supervised institution that is a clearing member client must use the methodologies described in paragraph (b) of this section to calculate risk-weighted assets for a cleared transaction.

(2) Clearing members. An FDIC-supervised institution that is a clearing member must use the methodologies described in paragraph (c) of this section to calculate its risk-weighted assets for a cleared transaction and paragraph (d) of this section to calculate its risk-weighted assets for its default fund contribution to a CCP.

(3) Alternate requirements. Notwithstanding any other provision of this section, an advanced approaches FDIC-supervised institution or a FDIC-supervised institution that is not an advanced approaches FDIC-supervised institution and that has elected to use SA-CCR under § 324.34(a)(1) must apply § 324.133 to its derivative contracts that are cleared transactions rather than this section.

(b) Clearing member client FDIC-supervised institutions —

(1) Risk-weighted assets for cleared transactions.

(i) To determine the risk-weighted asset amount for a cleared transaction, an FDIC-supervised institution that is a clearing member client must multiply the trade exposure amount for the cleared transaction, calculated in accordance with paragraph (b)(2) of this section, by the risk weight appropriate for the cleared transaction, determined in accordance with paragraph (b)(3) of this section.

(ii) A clearing member client FDIC-supervised institution's total risk-weighted assets for cleared transactions is the sum of the risk-weighted asset amounts for all its cleared transactions.

(2) Trade exposure amount.

(i) For a cleared transaction that is either a derivative contract or a netting set of derivative contracts, the trade exposure amount equals:

(A) The exposure amount for the derivative contract or netting set of derivative contracts, calculated using the methodology used to calculate exposure amount for OTC derivative contracts under § 324.34; plus

(B) The fair value of the collateral posted by the clearing member client FDIC-supervised institution and held by the CCP, clearing member, or custodian in a manner that is not bankruptcy remote.

(ii) For a cleared transaction that is a repo-style transaction or netting set of repo-style transactions, the trade exposure amount equals:

(A) The exposure amount for the repo-style transaction calculated using the methodologies under § 324.37(c); plus

(B) The fair value of the collateral posted by the clearing member client FDIC-supervised institution and held by the CCP, clearing member, or custodian in a manner that is not bankruptcy remote.

(3) Cleared transaction risk weights.

(i) For a cleared transaction with a QCCP, a clearing member client FDIC-supervised institution must apply a risk weight of:

(A) 2 percent if the collateral posted by the FDIC-supervised institution to the QCCP or clearing member is subject to an arrangement that prevents any losses to the clearing member client FDIC-supervised institution due to the joint default or a concurrent insolvency, liquidation, or receivership proceeding of the clearing member and any other clearing member clients of the clearing member; and the clearing member client FDIC-supervised institution has conducted sufficient legal review to conclude with a well-founded basis (and maintains sufficient written documentation of that legal review) that in the event of a legal challenge (including one resulting from an event of default or from liquidation, insolvency, or receivership proceedings) the relevant court and administrative authorities would find the arrangements to be legal, valid, binding and enforceable under the law of the relevant jurisdictions; or

(B) 4 percent if the requirements of § 324.35(b)(3)(A) are not met.

(ii) For a cleared transaction with a CCP that is not a QCCP, a clearing member client FDIC-supervised institution must apply the risk weight appropriate for the CCP according to this subpart D.

(4) Collateral.

(i) Notwithstanding any other requirements in this section, collateral posted by a clearing member client FDIC-supervised institution that is held by a custodian (in its capacity as custodian) in a manner that is bankruptcy remote from the CCP, clearing member, and other clearing member clients of the clearing member, is not subject to a capital requirement under this section.

(ii) A clearing member client FDIC-supervised institution must calculate a risk-weighted asset amount for any collateral provided to a CCP, clearing member, or custodian in connection with a cleared transaction in accordance with the requirements under this subpart D.

(c) Clearing member FDIC-supervised institutions —

(1) Risk-weighted assets for cleared transactions.

(i) To determine the risk-weighted asset amount for a cleared transaction, a clearing member FDIC-supervised institution must multiply the trade exposure amount for the cleared transaction, calculated in accordance with paragraph (c)(2) of this section, by the risk weight appropriate for the cleared transaction, determined in accordance with paragraph (c)(3) of this section.

(ii) A clearing member FDIC-supervised institution's total risk-weighted assets for cleared transactions is the sum of the risk-weighted asset amounts for all of its cleared transactions.

(2) Trade exposure amount. A clearing member FDIC-supervised institution must calculate its trade exposure amount for a cleared transaction as follows:

(i) For a cleared transaction that is either a derivative contract or a netting set of derivative contracts, the trade exposure amount equals:

(A) The exposure amount for the derivative contract, calculated using the methodology to calculate exposure amount for OTC derivative contracts under § 324.34; plus

(B) The fair value of the collateral posted by the clearing member FDIC-supervised institution and held by the CCP in a manner that is not bankruptcy remote.

(ii) For a cleared transaction that is a repo-style transaction or netting set of repo-style transactions, trade exposure amount equals:

(A) The exposure amount for repo-style transactions calculated using methodologies under § 324.37(c); plus

(B) The fair value of the collateral posted by the clearing member FDIC-supervised institution and held by the CCP in a manner that is not bankruptcy remote.

(3) Cleared transaction risk weight.

(i) A clearing member FDIC-supervised institution must apply a risk weight of 2 percent to the trade exposure amount for a cleared transaction with a QCCP.

(ii) For a cleared transaction with a CCP that is not a QCCP, a clearing member FDIC-supervised institution must apply the risk weight appropriate for the CCP according to this subpart D.

(iii) Notwithstanding paragraphs (c)(3)(i) and (ii) of this section, a clearing member FDIC-supervised institution may apply a risk weight of zero percent to the trade exposure amount for a cleared transaction with a CCP where the clearing member FDIC-supervised institution is acting as a financial intermediary on behalf of a clearing member client, the transaction offsets another transaction that satisfies the requirements set forth in § 324.3(a), and the clearing member FDIC-supervised institution is not obligated to reimburse the clearing member client in the event of the CCP default.

(4) Collateral.

(i) Notwithstanding any other requirement in this section, collateral posted by a clearing member FDIC-supervised institution that is held by a custodian in a manner that is bankruptcy remote from the CCP is not subject to a capital requirement under this section.

(ii) A clearing member FDIC-supervised institution must calculate a risk-weighted asset amount for any collateral provided to a CCP, clearing member, or a custodian in connection with a cleared transaction in accordance with requirements under this subpart D.

(d) Default fund contributions —

(1) General requirement. A clearing member FDIC-supervised institution must determine the risk-weighted asset amount for a default fund contribution to a CCP at least quarterly, or more frequently if, in the opinion of the FDIC-supervised institution or the FDIC, there is a material change in the financial condition of the CCP.

(2) Risk-weighted asset amount for default fund contributions to non-qualifying CCPs. A clearing member FDIC-supervised institution's risk-weighted asset amount for default fund contributions to CCPs that are not QCCPs equals the sum of such default fund contributions multiplied by 1,250 percent, or an amount determined by the FDIC, based on factors such as size, structure and membership characteristics of the CCP and riskiness of its transactions, in cases where such default fund contributions may be unlimited.

(3) Risk-weighted asset amount for default fund contributions to QCCP s. A clearing member FDIC-supervised institution's risk-weighted asset amount for default fund contributions to QCCPs equals the sum of its capital requirement, KCM for each QCCP, as calculated under the methodology set forth in paragraphs (d)(3)(i) through (iii) of this section (Method 1), multiplied by 1,250 percent or in paragraph (d)(3)(iv) of this section (Method 2).

(i) Method 1. The hypothetical capital requirement of a QCCP (KCCP) equals:

Where

(A) EBRMi equals the exposure amount for each transaction cleared through the QCCP by clearing member i, calculated in accordance with § 324.34 for OTC derivative contracts and § 324.37(c)(2) for repo-style transactions, provided that:

(1) For purposes of this section, in calculating the exposure amount the FDIC-supervised institution may replace the formula provided in § 324.34(a)(2)(ii) with the following: Anet = (0.15 × Agross) + (0.85 × NGR × Agross); and

(2) For option derivative contracts that are cleared transactions, the PFE described in § 324.34(a)(1)(ii) must be adjusted by multiplying the notional principal amount of the derivative contract by the appropriate conversion factor in Table 1 to § 324.34 and the absolute value of the option's delta, that is, the ratio of the change in the value of the derivative contract to the corresponding change in the price of the underlying asset.

(3) For repo-style transactions, when applying § 324.37(c)(2), the FDIC-supervised institution must use the methodology in § 324.37(c)(3);

(B) VMi equals any collateral posted by clearing member i to the QCCP that it is entitled to receive from the QCCP, but has not yet received, and any collateral that the QCCP has actually received from clearing member i;

(C) IMi equals the collateral posted as initial margin by clearing member i to the QCCP;

(D) DFi equals the funded portion of clearing member i's default fund contribution that will be applied to reduce the QCCP's loss upon a default by clearing member i;

(E) RW equals 20 percent, except when the FDIC has determined that a higher risk weight is more appropriate based on the specific characteristics of the QCCP and its clearing members; and

(F) Where a QCCP has provided its KCCP, an FDIC-supervised institution must rely on such disclosed figure instead of calculating KCCP under this paragraph (d), unless the FDIC-supervised institution determines that a more conservative figure is appropriate based on the nature, structure, or characteristics of the QCCP.

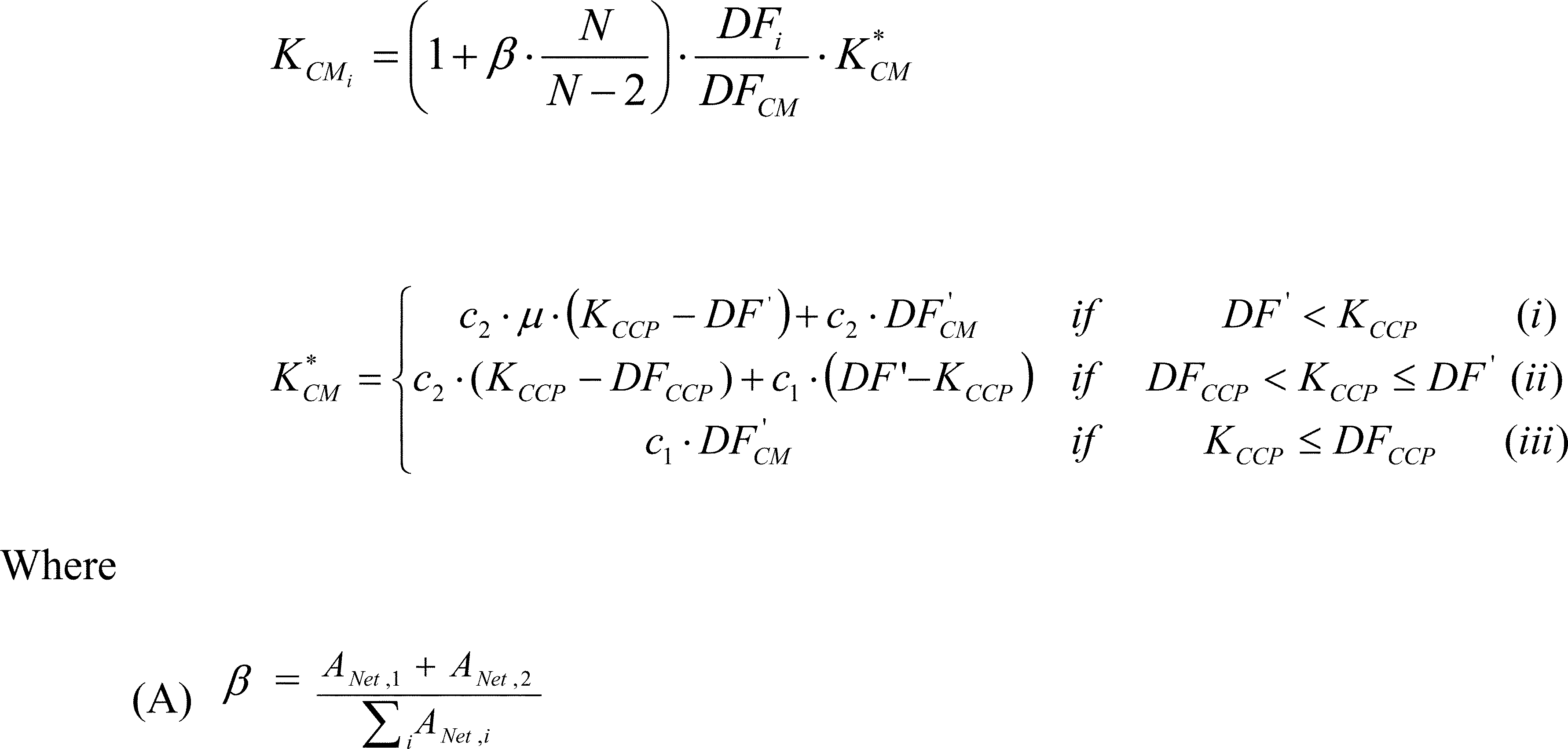

(ii) For an FDIC-supervised institution that is a clearing member of a QCCP with a default fund supported by funded commitments, KCM equals:

(A) Subscripts 1 and 2 denote the clearing members with the two largest ANet values. For purposes of this paragraph (d), for derivatives ANet is defined in § 324.34(a)(2)(ii) and for repo-style transactions, ANet means the exposure amount as defined in § 324.37(c)(2) using the methodology in § 324.37(c)(3);

(B) N equals the number of clearing members in the QCCP;

(C) DFCCP equals the QCCP's own funds and other financial resources that would be used to cover its losses before clearing members' default fund contributions are used to cover losses;

(D) DFCM equals funded default fund contributions from all clearing members and any other clearing member contributed financial resources that are available to absorb mutualized QCCP losses;

(E) DF = DFCCP + DFCM (that is, the total funded default fund contribution);

Where

(1) DFi equals the FDIC-supervised institution's unfunded commitment to the default fund;

(2) DFCM equals the total of all clearing members' unfunded commitment to the default fund; and

(3) K*CM as defined in paragraph (d)(3)(ii) of this section.

(B) For an FDIC-supervised institution that is a clearing member of a QCCP with a default fund supported by unfunded commitments and is unable to calculate KCM using the methodology described in paragraph (d)(3)(iii) of this section, KCM equals:

Where

(1) IMi = the FDIC-supervised institution's initial margin posted to the QCCP;

(2) IMCM equals the total of initial margin posted to the QCCP; and

(3) K*CM as defined in paragraph (d)(3)(ii) of this section.

(iv) Method 2. A clearing member FDIC-supervised institution's risk-weighted asset amount for its default fund contribution to a QCCP, RWADF, equals:

RWADF = Min {12.5 * DF; 0.18 * TE}

Where

(A) TE equals the FDIC-supervised institution's trade exposure amount to the QCCP, calculated according to § 324.35(c)(2);

(B) DF equals the funded portion of the FDIC-supervised institution's default fund contribution to the QCCP.

(4) Total risk-weighted assets for default fund contributions. Total risk-weighted assets for default fund contributions is the sum of a clearing member FDIC-supervised institution's risk-weighted assets for all of its default fund contributions to all CCPs of which the FDIC-supervised institution is a clearing member.

[78 FR 55471, Sept. 10, 2013, as amended at 79 FR 20760, Apr. 14, 2014; 84 FR 35277, July 22, 2019; 85 FR 4433, Jan. 24, 2020]

§ 324.36 Guarantees and credit derivatives: Substitution treatment.

(a) Scope —

(1) General. An FDIC-supervised institution may recognize the credit risk mitigation benefits of an eligible guarantee or eligible credit derivative by substituting the risk weight associated with the protection provider for the risk weight assigned to an exposure, as provided under this section.

(2) This section applies to exposures for which:

(i) Credit risk is fully covered by an eligible guarantee or eligible credit derivative; or

(ii) Credit risk is covered on a pro rata basis (that is, on a basis in which the FDIC-supervised institution and the protection provider share losses proportionately) by an eligible guarantee or eligible credit derivative.

(3) Exposures on which there is a tranching of credit risk (reflecting at least two different levels of seniority) generally are securitization exposures subject to §§ 324.41 through 324.45.

(4) If multiple eligible guarantees or eligible credit derivatives cover a single exposure described in this section, an FDIC-supervised institution may treat the hedged exposure as multiple separate exposures each covered by a single eligible guarantee or eligible credit derivative and may calculate a separate risk-weighted asset amount for each separate exposure as described in paragraph (c) of this section.

(5) If a single eligible guarantee or eligible credit derivative covers multiple hedged exposures described in paragraph (a)(2) of this section, an FDIC-supervised institution must treat each hedged exposure as covered by a separate eligible guarantee or eligible credit derivative and must calculate a separate risk-weighted asset amount for each exposure as described in paragraph (c) of this section.

(b) Rules of recognition.

(1) An FDIC-supervised institution may only recognize the credit risk mitigation benefits of eligible guarantees and eligible credit derivatives.

(2) An FDIC-supervised institution may only recognize the credit risk mitigation benefits of an eligible credit derivative to hedge an exposure that is different from the credit derivative's reference exposure used for determining the derivative's cash settlement value, deliverable obligation, or occurrence of a credit event if:

(i) The reference exposure ranks pari passu with, or is subordinated to, the hedged exposure; and

(ii) The reference exposure and the hedged exposure are to the same legal entity, and legally enforceable cross-default or cross-acceleration clauses are in place to ensure payments under the credit derivative are triggered when the obligated party of the hedged exposure fails to pay under the terms of the hedged exposure.

(c) Substitution approach —

(1) Full coverage. If an eligible guarantee or eligible credit derivative meets the conditions in paragraphs (a) and (b) of this section and the protection amount (P) of the guarantee or credit derivative is greater than or equal to the exposure amount of the hedged exposure, an FDIC-supervised institution may recognize the guarantee or credit derivative in determining the risk-weighted asset amount for the hedged exposure by substituting the risk weight applicable to the guarantor or credit derivative protection provider under this subpart D for the risk weight assigned to the exposure.

(2) Partial coverage. If an eligible guarantee or eligible credit derivative meets the conditions in paragraphs (a) and (b) of this section and the protection amount (P) of the guarantee or credit derivative is less than the exposure amount of the hedged exposure, the FDIC-supervised institution must treat the hedged exposure as two separate exposures (protected and unprotected) in order to recognize the credit risk mitigation benefit of the guarantee or credit derivative.

(i) The FDIC-supervised institution may calculate the risk-weighted asset amount for the protected exposure under this subpart D, where the applicable risk weight is the risk weight applicable to the guarantor or credit derivative protection provider.

(ii) The FDIC-supervised institution must calculate the risk-weighted asset amount for the unprotected exposure under this subpart D, where the applicable risk weight is that of the unprotected portion of the hedged exposure.

(iii) The treatment provided in this section is applicable when the credit risk of an exposure is covered on a partial pro rata basis and may be applicable when an adjustment is made to the effective notional amount of the guarantee or credit derivative under paragraphs (d), (e), or (f) of this section.

(d) Maturity mismatch adjustment.

(1) An FDIC-supervised institution that recognizes an eligible guarantee or eligible credit derivative in determining the risk-weighted asset amount for a hedged exposure must adjust the effective notional amount of the credit risk mitigant to reflect any maturity mismatch between the hedged exposure and the credit risk mitigant.

(2) A maturity mismatch occurs when the residual maturity of a credit risk mitigant is less than that of the hedged exposure(s).

(3) The residual maturity of a hedged exposure is the longest possible remaining time before the obligated party of the hedged exposure is scheduled to fulfil its obligation on the hedged exposure. If a credit risk mitigant has embedded options that may reduce its term, the FDIC-supervised institution (protection purchaser) must use the shortest possible residual maturity for the credit risk mitigant. If a call is at the discretion of the protection provider, the residual maturity of the credit risk mitigant is at the first call date. If the call is at the discretion of the FDIC-supervised institution (protection purchaser), but the terms of the arrangement at origination of the credit risk mitigant contain a positive incentive for the FDIC-supervised institution to call the transaction before contractual maturity, the remaining time to the first call date is the residual maturity of the credit risk mitigant.

(4) A credit risk mitigant with a maturity mismatch may be recognized only if its original maturity is greater than or equal to one year and its residual maturity is greater than three months.

(5) When a maturity mismatch exists, the FDIC-supervised institution must apply the following adjustment to reduce the effective notional amount of the credit risk mitigant: Pm = E × (t-0.25)/(T-0.25), where:

(i) Pm equals effective notional amount of the credit risk mitigant, adjusted for maturity mismatch;

(ii) E equals effective notional amount of the credit risk mitigant;

(iii) t equals the lesser of T or the residual maturity of the credit risk mitigant, expressed in years; and

(iv) T equals the lesser of five or the residual maturity of the hedged exposure, expressed in years.

(e) Adjustment for credit derivatives without restructuring as a credit event. If an FDIC-supervised institution recognizes an eligible credit derivative that does not include as a credit event a restructuring of the hedged exposure involving forgiveness or postponement of principal, interest, or fees that results in a credit loss event (that is, a charge-off, specific provision, or other similar debit to the profit and loss account), the FDIC-supervised institution must apply the following adjustment to reduce the effective notional amount of the credit derivative: Pr = Pm × 0.60, where:

(1) Pr equals effective notional amount of the credit risk mitigant, adjusted for lack of restructuring event (and maturity mismatch, if applicable); and

(2) Pm equals effective notional amount of the credit risk mitigant (adjusted for maturity mismatch, if applicable).

(f) Currency mismatch adjustment.

(1) If an FDIC-supervised institution recognizes an eligible guarantee or eligible credit derivative that is denominated in a currency different from that in which the hedged exposure is denominated, the FDIC-supervised institution must apply the following formula to the effective notional amount of the guarantee or credit derivative: Pc = Pr × (1-HFX), where:

(i) Pc equals effective notional amount of the credit risk mitigant, adjusted for currency mismatch (and maturity mismatch and lack of restructuring event, if applicable);

(ii) Pr equals effective notional amount of the credit risk mitigant (adjusted for maturity mismatch and lack of restructuring event, if applicable); and

(iii) HFX equals haircut appropriate for the currency mismatch between the credit risk mitigant and the hedged exposure.

(2) An FDIC-supervised institution must set HFX equal to eight percent unless it qualifies for the use of and uses its own internal estimates of foreign exchange volatility based on a ten-business-day holding period. An FDIC-supervised institution qualifies for the use of its own internal estimates of foreign exchange volatility if it qualifies for the use of its own-estimates haircuts in § 324.37(c)(4).

(3) An FDIC-supervised institution must adjust HFX calculated in paragraph (f)(2) of this section upward if the FDIC-supervised institution revalues the guarantee or credit derivative less frequently than once every 10 business days using the following square root of time formula:

[78 FR 55471, Sept. 10, 2013, as amended at 84 FR 35277, July 22, 2019]

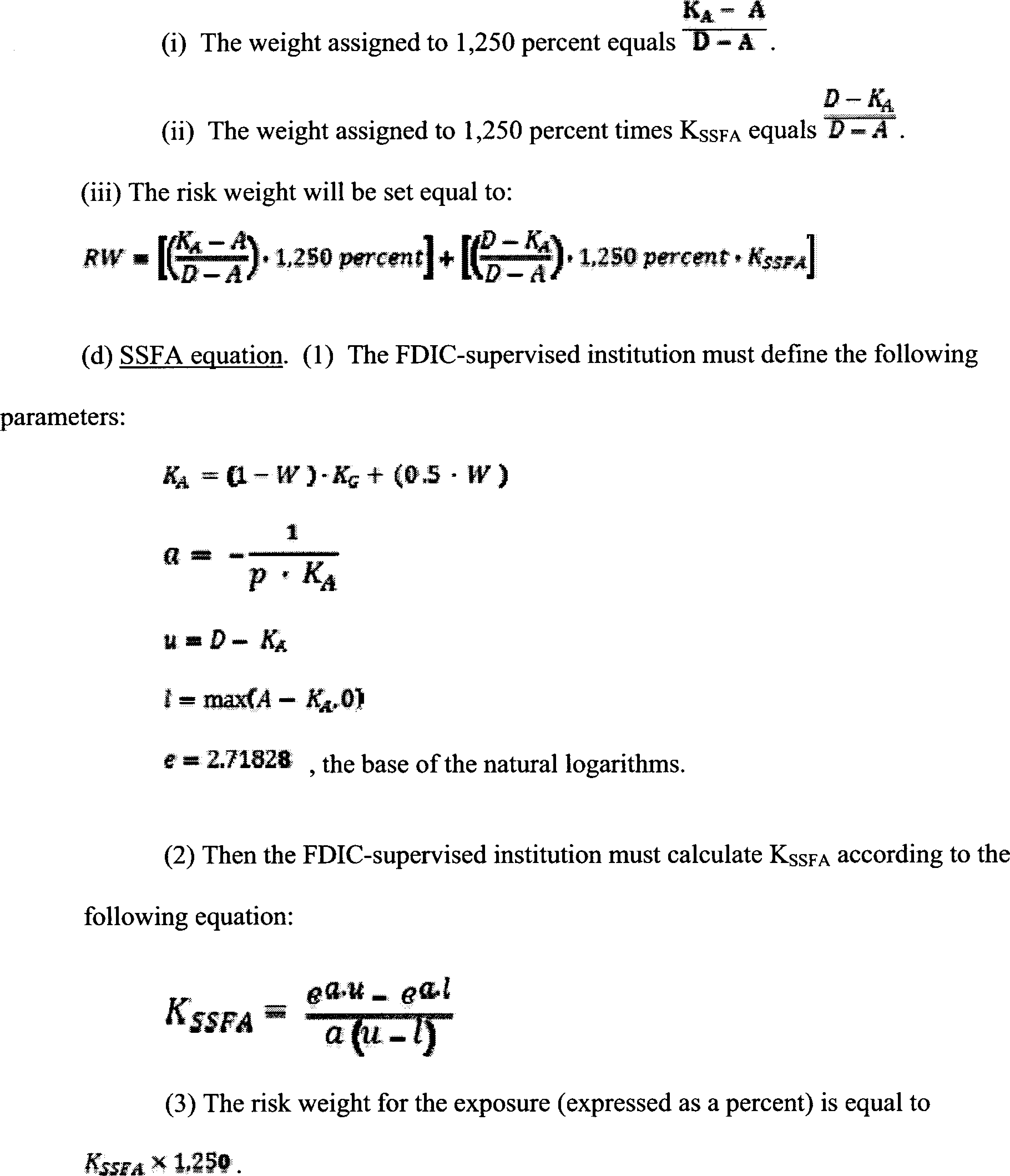

§ 324.37 Collateralized transactions.

(a) General.

(1) To recognize the risk-mitigating effects of financial collateral, an FDIC-supervised institution may use:

(i) The simple approach in paragraph (b) of this section for any exposure; or

(ii) The collateral haircut approach in paragraph (c) of this section for repo-style transactions, eligible margin loans, collateralized derivative contracts, and single-product netting sets of such transactions.

(2) An FDIC-supervised institution may use any approach described in this section that is valid for a particular type of exposure or transaction; however, it must use the same approach for similar exposures or transactions.

(b) The simple approach —

(1) General requirements.

(i) An FDIC-supervised institution may recognize the credit risk mitigation benefits of financial collateral that secures any exposure.

(ii) To qualify for the simple approach, the financial collateral must meet the following requirements:

(A) The collateral must be subject to a collateral agreement for at least the life of the exposure;

(B) The collateral must be revalued at least every six months; and

(C) The collateral (other than gold) and the exposure must be denominated in the same currency.

(2) Risk weight substitution.

(i) An FDIC-supervised institution may apply a risk weight to the portion of an exposure that is secured by the fair value of financial collateral (that meets the requirements of paragraph (b)(1) of this section) based on the risk weight assigned to the collateral under this subpart D. For repurchase agreements, reverse repurchase agreements, and securities lending and borrowing transactions, the collateral is the instruments, gold, and cash the FDIC-supervised institution has borrowed, purchased subject to resale, or taken as collateral from the counterparty under the transaction. Except as provided in paragraph (b)(3) of this section, the risk weight assigned to the collateralized portion of the exposure may not be less than 20 percent.

(ii) An FDIC-supervised institution must apply a risk weight to the unsecured portion of the exposure based on the risk weight applicable to the exposure under this subpart.

(3) Exceptions to the 20 percent risk-weight floor and other requirements. Notwithstanding paragraph (b)(2)(i) of this section:

(i) An FDIC-supervised institution may assign a zero percent risk weight to an exposure to an OTC derivative contract that is marked-to-market on a daily basis and subject to a daily margin maintenance requirement, to the extent the contract is collateralized by cash on deposit.

(ii) An FDIC-supervised institution may assign a 10 percent risk weight to an exposure to an OTC derivative contract that is marked-to-market daily and subject to a daily margin maintenance requirement, to the extent that the contract is collateralized by an exposure to a sovereign that qualifies for a zero percent risk weight under § 324.32.

(iii) An FDIC-supervised institution may assign a zero percent risk weight to the collateralized portion of an exposure where:

(A) The financial collateral is cash on deposit; or

(B) The financial collateral is an exposure to a sovereign that qualifies for a zero percent risk weight under § 324.32, and the FDIC-supervised institution has discounted the fair value of the collateral by 20 percent.

(c) Collateral haircut approach —

(1) General. An FDIC-supervised institution may recognize the credit risk mitigation benefits of financial collateral that secures an eligible margin loan, repo-style transaction, collateralized derivative contract, or single-product netting set of such transactions, and of any collateral that secures a repo-style transaction that is included in the FDIC-supervised institution's VaR-based measure under subpart F of this part by using the collateral haircut approach in this section. An FDIC-supervised institution may use the standard supervisory haircuts in paragraph (c)(3) of this section or, with prior written approval of the FDIC, its own estimates of haircuts according to paragraph (c)(4) of this section.

(2) Exposure amount equation. An FDIC-supervised institution must determine the exposure amount for an eligible margin loan, repo-style transaction, collateralized derivative contract, or a single-product netting set of such transactions by setting the exposure amount equal to max {0, [(∑E − ∑C) + ∑(Es × Hs) + ∑(Efx × Hfx)]}, where:

(i)

(A) For eligible margin loans and repo-style transactions and netting sets thereof, ∑E equals the value of the exposure (the sum of the current fair values of all instruments, gold, and cash the FDIC-supervised institution has lent, sold subject to repurchase, or posted as collateral to the counterparty under the transaction (or netting set)); and

(B) For collateralized derivative contracts and netting sets thereof, ∑E equals the exposure amount of the OTC derivative contract (or netting set) calculated under § 324.34(b)(1) or (2).

(ii) ∑C equals the value of the collateral (the sum of the current fair values of all instruments, gold and cash the FDIC-supervised institution has borrowed, purchased subject to resale, or taken as collateral from the counterparty under the transaction (or netting set));

(iii) Es equals the absolute value of the net position in a given instrument or in gold (where the net position in the instrument or gold equals the sum of the current fair values of the instrument or gold the FDIC-supervised institution has lent, sold subject to repurchase, or posted as collateral to the counterparty minus the sum of the current fair values of that same instrument or gold the FDIC-supervised institution has borrowed, purchased subject to resale, or taken as collateral from the counterparty);

(iv) Hs equals the market price volatility haircut appropriate to the instrument or gold referenced in Es;

(v) Efx equals the absolute value of the net position of instruments and cash in a currency that is different from the settlement currency (where the net position in a given currency equals the sum of the current fair values of any instruments or cash in the currency the FDIC-supervised institution has lent, sold subject to repurchase, or posted as collateral to the counterparty minus the sum of the current fair values of any instruments or cash in the currency the FDIC-supervised institution has borrowed, purchased subject to resale, or taken as collateral from the counterparty); and

(vi) Hfx equals the haircut appropriate to the mismatch between the currency referenced in Efx and the settlement currency.

(3) Standard supervisory haircuts.

(i) An FDIC-supervised institution must use the haircuts for market price volatility (Hs) provided in Table 1 to § 324.37, as adjusted in certain circumstances in accordance with the requirements of paragraphs (c)(3)(iii) and (iv) of this section.

Table 1 to § 324.37—Standard Supervisory Market Price Volatility Haircuts1

| Residual maturity | Haircut (in percent) assigned based on: | Investment grade securitization exposures (in percent) |

|||||

|---|---|---|---|---|---|---|---|

| Sovereign issuers risk weight under § 324.32 (in percent)2 |

Non-sovereign issuers risk weight under § 324.32 (in percent) |

||||||

| Zero | 20 or 50 | 100 | 20 | ||||

| Less than or equal to 1 year | 0.5 | 1.0 | 15.0 | 1.0 | 2.0 | 4.0 | 4.0 |

| Greater than 1 year and less than or equal to 5 years | 2.0 | 3.0 | 15.0 | 4.0 | 6.0 | 8.0 | 12.0 |

| Greater than 5 years | 4.0 | 6.0 | 15.0 | 8.0 | 12.0 | 16.0 | 24.0 |

| Main index equities (including convertible bonds) and gold | 15.0 | ||||||

| Other publicly traded equities (including convertible bonds) | 25.0 | ||||||

| Mutual funds | Highest haircut applicable to any security in which the fund can invest. | ||||||

| Cash collateral held | Zero | ||||||

| Other exposure types | 25.0 | ||||||

(ii) For currency mismatches, an FDIC-supervised institution must use a haircut for foreign exchange rate volatility (Hfx) of 8.0 percent, as adjusted in certain circumstances under paragraphs (c)(3)(iii) and (iv) of this section.

(iii) For repo-style transactions and client-facing derivative transactions, a FDIC-supervised institution may multiply the standard supervisory haircuts provided in paragraphs (c)(3)(i) and (ii) of this section by the square root of 1⁄2 (which equals 0.707107). For client-facing derivative transactions, if a larger scaling factor is applied under § 324.34(f), the same factor must be used to adjust the supervisory haircuts.

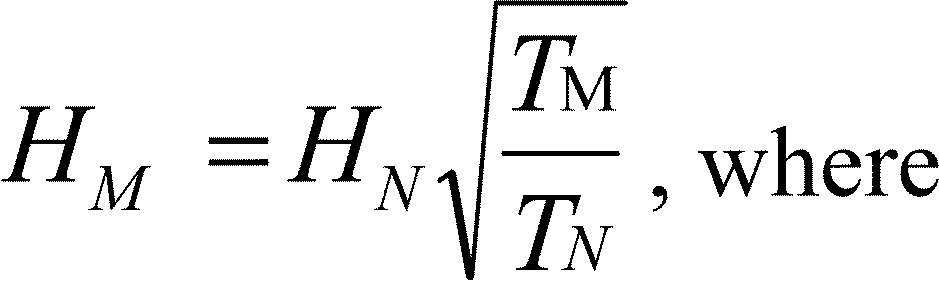

(iv) If the number of trades in a netting set exceeds 5,000 at any time during a quarter, an FDIC-supervised institution must adjust the supervisory haircuts provided in paragraphs (c)(3)(i) and (ii) of this section upward on the basis of a holding period of twenty business days for the following quarter except in the calculation of the exposure amount for purposes of § 324.35. If a netting set contains one or more trades involving illiquid collateral or an OTC derivative that cannot be easily replaced, an FDIC-supervised institution must adjust the supervisory haircuts upward on the basis of a holding period of twenty business days. If over the two previous quarters more than two margin disputes on a netting set have occurred that lasted more than the holding period, then the FDIC-supervised institution must adjust the supervisory haircuts upward for that netting set on the basis of a holding period that is at least two times the minimum holding period for that netting set. An FDIC-supervised institution must adjust the standard supervisory haircuts upward using the following formula:

(A) TM equals a holding period of longer than 10 business days for eligible margin loans and derivative contracts other than client-facing derivative transactions or longer than 5 business days for repo-style transactions and client-facing derivative transactions;

(B) HS equals the standard supervisory haircut; and

(C) TS equals 10 business days for eligible margin loans and derivative contracts other than client-facing derivative transactions or 5 business days for repo-style transactions and client-facing derivative transactions.

(v) If the instrument an FDIC-supervised institution has lent, sold subject to repurchase, or posted as collateral does not meet the definition of financial collateral, the FDIC-supervised institution must use a 25.0 percent haircut for market price volatility (Hs).

(4) Own internal estimates for haircuts. With the prior written approval of the FDIC, an FDIC-supervised institution may calculate haircuts (Hs and Hfx) using its own internal estimates of the volatilities of market prices and foreign exchange rates:

(i) To receive FDIC approval to use its own internal estimates, an FDIC-supervised institution must satisfy the following minimum standards:

(A) An FDIC-supervised institution must use a 99th percentile one-tailed confidence interval.

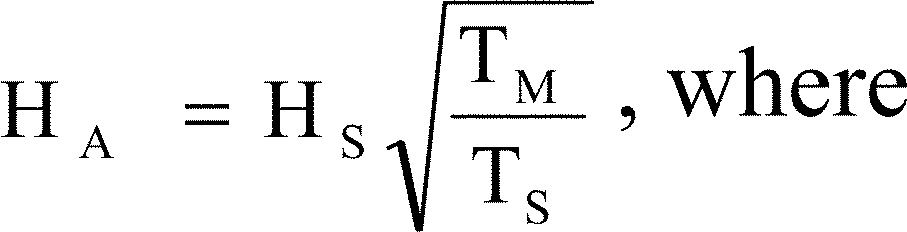

(B) The minimum holding period for a repo-style transaction and client-facing derivative transaction is five business days and for an eligible margin loan and a derivative contract other than a client-facing derivative transaction is ten business days except for transactions or netting sets for which paragraph (c)(4)(i)(C) of this section applies. When a FDIC-supervised institution calculates an own-estimates haircut on a TN-day holding period, which is different from the minimum holding period for the transaction type, the applicable haircut (HM) is calculated using the following square root of time formula:

(1) TM equals 5 for repo-style transactions and client-facing derivative transactions and 10 for eligible margin loans and derivative contracts other than client-facing derivative transactions;

(2) TN equals the holding period used by the FDIC-supervised institution to derive HN; and

(3) HN equals the haircut based on the holding period TN.

(C) If the number of trades in a netting set exceeds 5,000 at any time during a quarter, an FDIC-supervised institution must calculate the haircut using a minimum holding period of twenty business days for the following quarter except in the calculation of the exposure amount for purposes of § 324.35. If a netting set contains one or more trades involving illiquid collateral or an OTC derivative that cannot be easily replaced, an FDIC-supervised institution must calculate the haircut using a minimum holding period of twenty business days. If over the two previous quarters more than two margin disputes on a netting set have occurred that lasted more than the holding period, then the FDIC-supervised institution must calculate the haircut for transactions in that netting set on the basis of a holding period that is at least two times the minimum holding period for that netting set.

(D) An FDIC-supervised institution is required to calculate its own internal estimates with inputs calibrated to historical data from a continuous 12-month period that reflects a period of significant financial stress appropriate to the security or category of securities.

(E) An FDIC-supervised institution must have policies and procedures that describe how it determines the period of significant financial stress used to calculate the FDIC-supervised institution's own internal estimates for haircuts under this section and must be able to provide empirical support for the period used. The FDIC-supervised institution must obtain the prior approval of the FDIC for, and notify the FDIC if the FDIC-supervised institution makes any material changes to, these policies and procedures.

(F) Nothing in this section prevents the FDIC from requiring an FDIC-supervised institution to use a different period of significant financial stress in the calculation of own internal estimates for haircuts.

(G) An FDIC-supervised institution must update its data sets and calculate haircuts no less frequently than quarterly and must also reassess data sets and haircuts whenever market prices change materially.

(ii) With respect to debt securities that are investment grade, an FDIC-supervised institution may calculate haircuts for categories of securities. For a category of securities, the FDIC-supervised institution must calculate the haircut on the basis of internal volatility estimates for securities in that category that are representative of the securities in that category that the FDIC-supervised institution has lent, sold subject to repurchase, posted as collateral, borrowed, purchased subject to resale, or taken as collateral. In determining relevant categories, the FDIC-supervised institution must at a minimum take into account:

(A) The type of issuer of the security;

(B) The credit quality of the security;

(C) The maturity of the security; and

(D) The interest rate sensitivity of the security.

(iii) With respect to debt securities that are not investment grade and equity securities, an FDIC-supervised institution must calculate a separate haircut for each individual security.

(iv) Where an exposure or collateral (whether in the form of cash or securities) is denominated in a currency that differs from the settlement currency, the FDIC-supervised institution must calculate a separate currency mismatch haircut for its net position in each mismatched currency based on estimated volatilities of foreign exchange rates between the mismatched currency and the settlement currency.

(v) An FDIC-supervised institution's own estimates of market price and foreign exchange rate volatilities may not take into account the correlations among securities and foreign exchange rates on either the exposure or collateral side of a transaction (or netting set) or the correlations among securities and foreign exchange rates between the exposure and collateral sides of the transaction (or netting set).

[78 FR 55471, Sept. 10, 2013, as amended at 79 FR 20760, Apr. 14, 2014; 84 FR 35277, July 22, 2019; 85 FR 4433, Jan. 24, 2020; 85 FR 57963, Sept. 17, 2020]

Risk-Weighted Assets for Unsettled Transactions

§ 324.38 Unsettled transactions.

(a) Definitions. For purposes of this section:

(1) Delivery-versus-payment (DvP) transaction means a securities or commodities transaction in which the buyer is obligated to make payment only if the seller has made delivery of the securities or commodities and the seller is obligated to deliver the securities or commodities only if the buyer has made payment.

(2) Payment-versus-payment (PvP) transaction means a foreign exchange transaction in which each counterparty is obligated to make a final transfer of one or more currencies only if the other counterparty has made a final transfer of one or more currencies.

(3) A transaction has a normal settlement period if the contractual settlement period for the transaction is equal to or less than the market standard for the instrument underlying the transaction and equal to or less than five business days.

(4) Positive current exposure of an FDIC-supervised institution for a transaction is the difference between the transaction value at the agreed settlement price and the current market price of the transaction, if the difference results in a credit exposure of the FDIC-supervised institution to the counterparty.

(b) Scope. This section applies to all transactions involving securities, foreign exchange instruments, and commodities that have a risk of delayed settlement or delivery. This section does not apply to:

(1) Cleared transactions that are marked-to-market daily and subject to daily receipt and payment of variation margin;

(2) Repo-style transactions, including unsettled repo-style transactions;

(3) One-way cash payments on OTC derivative contracts; or

(4) Transactions with a contractual settlement period that is longer than the normal settlement period (which are treated as OTC derivative contracts as provided in § 324.34).

(c) System-wide failures. In the case of a system-wide failure of a settlement, clearing system or central counterparty, the FDIC may waive risk-based capital requirements for unsettled and failed transactions until the situation is rectified.

(d) Delivery-versus-payment (DvP) and payment-versus-payment (PvP) transactions. An FDIC-supervised institution must hold risk-based capital against any DvP or PvP transaction with a normal settlement period if the FDIC-supervised institution's counterparty has not made delivery or payment within five business days after the settlement date. The FDIC-supervised institution must determine its risk-weighted asset amount for such a transaction by multiplying the positive current exposure of the transaction for the FDIC-supervised institution by the appropriate risk weight in Table 1 to § 324.38.

Table 1 to § 324.38—Risk Weights for Unsettled DvP and PvP Transactions

| Number of business days after contractual settlement date | Risk weight to be applied to positive current exposure (in percent) |

|---|---|

| From 5 to 15 | 100.0 |

| From 16 to 30 | 625.0 |

| From 31 to 45 | 937.5 |

| 46 or more | 1,250.0 |

(e) Non-DvP/non-PvP (non-delivery-versus-payment/non-payment-versus-payment) transactions.

(1) An FDIC-supervised institution must hold risk-based capital against any non-DvP/non-PvP transaction with a normal settlement period if the FDIC-supervised institution has delivered cash, securities, commodities, or currencies to its counterparty but has not received its corresponding deliverables by the end of the same business day. The FDIC-supervised institution must continue to hold risk-based capital against the transaction until the FDIC-supervised institution has received its corresponding deliverables.

(2) From the business day after the FDIC-supervised institution has made its delivery until five business days after the counterparty delivery is due, the FDIC-supervised institution must calculate the risk-weighted asset amount for the transaction by treating the current fair value of the deliverables owed to the FDIC-supervised institution as an exposure to the counterparty and using the applicable counterparty risk weight under this subpart D.

(3) If the FDIC-supervised institution has not received its deliverables by the fifth business day after counterparty delivery was due, the FDIC-supervised institution must assign a 1,250 percent risk weight to the current fair value of the deliverables owed to the FDIC-supervised institution.

(f) Total risk-weighted assets for unsettled transactions. Total risk-weighted assets for unsettled transactions is the sum of the risk-weighted asset amounts of all DvP, PvP, and non-DvP/non-PvP transactions.

[78 FR 55471, Sept. 10, 2013, as amended at 84 FR 35277, July 22, 2019]

§§ 324.39-324.40 [Reserved]

Risk-Weighted Assets for Securitization Exposures

§ 324.41 Operational requirements for securitization exposures.

(a) Operational criteria for traditional securitizations. An FDIC-supervised institution that transfers exposures it has originated or purchased to a securitization SPE or other third party in connection with a traditional securitization may exclude the exposures from the calculation of its risk-weighted assets only if each condition in this section is satisfied. An FDIC-supervised institution that meets these conditions must hold risk-based capital against any credit risk it retains in connection with the securitization. An FDIC-supervised institution that fails to meet these conditions must hold risk-based capital against the transferred exposures as if they had not been securitized and must deduct from common equity tier 1 capital any after-tax gain-on-sale resulting from the transaction. The conditions are:

(1) The exposures are not reported on the FDIC-supervised institution's consolidated balance sheet under GAAP;

(2) The FDIC-supervised institution has transferred to one or more third parties credit risk associated with the underlying exposures;